Why Your Teenager’s Impulsive Spending Is Not a Knowledge Problem

Here is a reality that catches many parents off guard: your teenager probably knows the basic rules of money. They understand that saving is good, that budgets exist, and that they should spend less than they receive.

Yet, we regularly see a distinct operational shift happen somewhere between primary and secondary school. At a primary school age, the financial relationship is straightforward. You sit your child down, explain simple boundaries, and they generally respond directly to those limits. But at the secondary school tier, you can provide those exact same explanations, use the exact same logic, and get wildly different, completely surprising results.

Perfect marks on a financial literacy worksheet do not automatically translate to responsible choices inside a crowded school canteen. When real-world decisions surprise or blindside us, it is rarely because our children lack structural ignorance. It is because money has stopped being a math problem—and has started being an identity problem.

If You’d Rather Watch The Video

The Core Misconception: Knowledge vs. Formation

The biggest mistake we can make as parents and educators is treating teenage spending as a sequence of transaction errors. Financial education that only reaches the mind will never reshape behavior.

In our school programmes across Singapore, we see this pattern repeatedly. We meet students who can perfectly recite definitions of budgeting, saving, and delayed gratification. However, when placed under real-time pressure, their choices tell a completely different story.

During a recent experiential school workshop, we ran a controlled board game simulation. One student gave all the right answers during our initial discussions, showing real intellectual capability. But the moment the simulation began, his actual choices shifted completely. He started taking on massive, high-risk loans that were completely unsupported by any assets or revenue. When gently questioned about his strategy, he looked at me confidently and insisted it was simply "good debt". At the end of the simulation, his choices led him straight to absolute financial ruin.

Thankfully, this happened inside a safe classroom environment rather than the real world. But it proved an essential principle: knowing the financial terms does not mean a young person possesses the maturity to apply them under pressure. To build real judgment, we have to look past the transaction itself and investigate the psychological engine driving it.

Decoding the Identity-Spending Loop

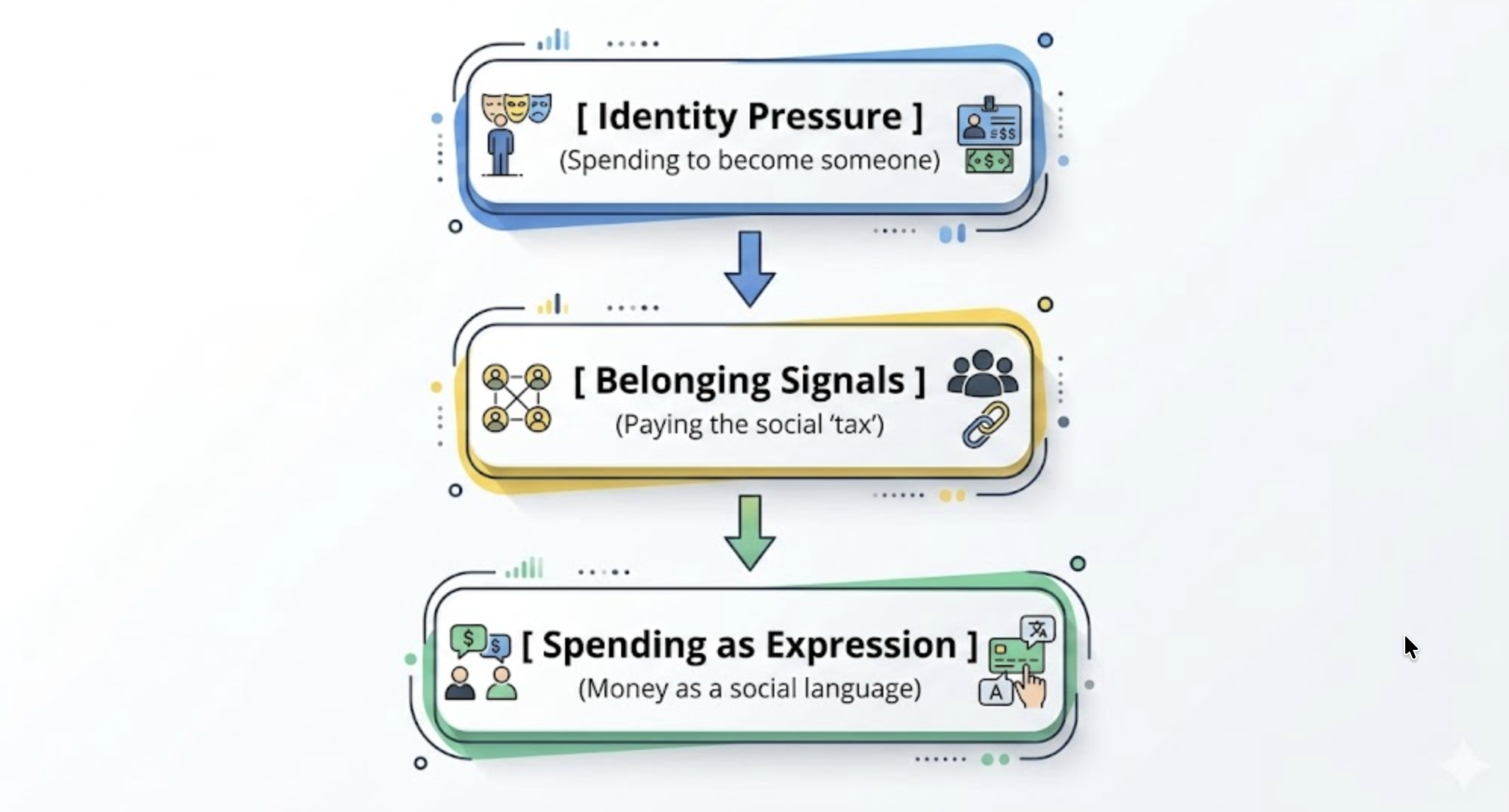

If your child is anywhere between thirteen and eighteen, their financial choices are largely directed by a framework we call the Identity-Spending Loop. This loop consists of three distinct layers. Once you learn to recognise them, you will never look at your teenager’s purchases the same way again.

1. Identity Pressure (Spending to Become Someone)

Adolescence is the core developmental stage of identity formation; it is not a collection of character flaws. The big question—"Who am I?"—is frequently answered through what teenagers choose to own, carry, and participate in.

Think about Singapore secondary school culture. The intense focus on specific schoolbag brands, particular phone models, or trendy branded water bottles is rarely about functionality. These are carefully calibrated social signals. The financial risk occurs when the identity a teenager is trying to build requires money they do not have, or habits they cannot sustain. Financial immaturity looks like spending money to feel like someone, rather than to acquire something useful.

2. Belonging Signals (Paying the "Belonging Tax")

Belonging is a non-negotiable force in a teenager's life, and it almost always carries a price tag. Peer groups define their boundaries through shared objects, digital experiences, and weekend activities. Having or not having these elements signals whether a child is safely in, or completely out.

From a teenager's perspective, spending their allowance to join a group activity is not frivolous or superficial—it feels entirely necessary. This is not materialism; it is belonging.

Many parents respond to this by saying, "True belonging doesn't depend on what you own." While that is a true principle, teenagers do not fully believe it yet because they haven't lived long enough to see it proven. You cannot defeat immediate peer pressure using abstract, theoretical statements. Peer pressure works through raw, lived daily experience.

3. Spending as Expression (Money as a Language)

By the time your teenager reaches fifteen or sixteen, money is no longer just a medium of exchange. It has become a language. They use it to express identity, personal taste, and perceived maturity—both to their peers and back to themselves.

This dynamic is incredibly resilient.

Looking back at my own youth, I clearly remember times when my friends planned to head out to specific locations. I knew exactly how much money was in my pocket, and I knew that joining them would mean losing my financial freedom to do anything else for the rest of the week. Yet, I consciously chose to spend it anyway. My desire to express that I belonged to that group mattered more to me than my individual comfort.

Similarly, when we observe youths today, their intense desire to stay connected causes them to make choices that push them to spend far more than they would like. If this underlying pattern is never addressed, the habit of using spending as a tool for self-expression grows up with them. They enter adulthood with a much larger income, met with vastly larger consequences.

Moving From Transaction to Transformation

How do we break the loop without creating unnecessary domestic friction? The shift begins by introducing a neutral, non-judgmental conversational checkpoint.

The next time your teenager comes to you with an unexpected or trendy spending request, pause the automatic lecture on budgeting. Instead, implement this single diagnostic question:

"Who else in your group has this?"

Do not deliver it as an accusation or a trap. Ask it as a genuine opening to understand their environment, and listen carefully to what their answer reveals. It allows you to identify whether the request is driven by functional utility or an underlying identity driver. It changes your role from an automated transaction approval engine into a thoughtful guide.

The 3-Step Action Plan For Families

To help your teenager build independent financial judgment that outlasts their peer environment, implement this three-step framework this week:

Step 1: Watch for the trigger, not just the transaction. Notice whether spending requests cluster heavily around major social transitions—such as starting a new CCA, joining a new group of friends, or entering a new school term. Recognising the context allows you to address the real identity question beneath the purchase.

Step 2: Train them to use an internal filter. Before every major spending conversation, encourage your teen to evaluate their request through a clear, three-part distinction: "Is this item something you need, something you want, or something you feel you should carry to fit in?" Naming the mechanism without shaming their character helps them separate social pressure from functional utility.

Step 3: Give them low-stakes practice with real money. Teenagers cannot build financial judgment without carrying real money decisions. Let them manage a bounded weekly or monthly allocation with genuine freedom—and genuine consequences. Let them feel the real-world friction of running out of money early while the stakes are still small and manageable. Supervised freedom, not constant surveillance, is how true maturity develops.

Our ultimate goal is not to stop teenagers from spending. The goal is to equip them with the independent judgment to make wise decisions—even when identity, belonging, and peer image are all standing in the room.

Join the Movement

At Leaven Academy, we partner with schools, educators, and families across Singapore to build real-world youth readiness and character maturity that goes beyond the academic curriculum.

If you want to help your youth develop the mindset, habits, and judgment needed to navigate real-world decisions responsibly, let’s begin a conversation.

Explore our frameworks: Visit Leaven Academy Contact Page to learn more about our experiential workshops.

Connect directly: Email our team at ernest@leavenacademy.com to discuss how we can support your school or community group.

FAQ Section

Q: My teenager already receives a fixed allowance but constantly asks for advances before the week ends. Should I give it to them?

No. When you step in to eliminate the consequence of running out of money, you transform financial freedom back into absolute financial supervision. Let them experience the natural friction of a zero balance while the stakes are low. It is better for them to experience a week without café snacks at age fourteen than absolute financial ruin as an adult.

Q: How can I tell if my child is materialistic or just trying to fit in?

Look closely at what happens after the purchase. Materialism centers on the possession of the item itself. A belonging signal, however, is about access to a social group. If your teen only uses or wears an item when they are interacting with a specific circle of friends, they are paying a temporary social "belonging tax", not displaying a permanent character flaw.

Q: Is the Identity-Spending Loop unique to secondary school students?

While identity-driven spending happens at all stages of life, it peaks in intensity during the secondary school years (ages 13 to 18). This is the exact developmental window where human beings naturally detach slightly from family structures to find their footing within peer groups. Money becomes one of the most accessible tools to bridge that gap.