Performer or Leader? 4 Signs Your Teenager Is Actually Trustworthy

Confidence isn't leadership. Here are four signs of trustworthy leadership — reliability, ownership, honesty, follow-through — parents can watch for in their teenager at home, with a practical step for each.

Why Leadership Titles Don't Build Leadership in Students

A prefect badge or CCA captaincy is not proof of leadership — it's permission to start practising it. Many school leadership systems treat titles as the finish line rather than the starting line. This article breaks down the three-part framework Singapore schools need to move student leaders from visibility to real, trustworthy responsibility.

Why Visible Students Aren't Always Your Best Leaders

and confident — but visibility is not the same as trustworthiness. This article introduces three practical tests Singapore schools can use to identify students who are genuinely ready for responsibility, not just comfortable in front of an audience.Why Money Behaviour Reveals More Than Money Habits

Most schools treat financial education as a subject. But the way students handle money is one of the clearest windows into how they handle responsibility more broadly. This article introduces the Maturity Signal Framework and explains what student money behaviour is actually telling schools — and what to do about it.

Why Financial Literacy Programmes Fail Singapore Students

Every year, thousands of Singapore students complete financial literacy programmes with strong quiz scores and flawless worksheets. And every year, the same gap appears two weeks later: the money is spent, the budget is forgotten, and the knowledge did not produce different behaviour. This article examines why — and what a formation-focused approach actually looks like in practice.

Why Your Teenager's Money Habits Are Already Forming

The first visible financial mistake your teenager makes is rarely the beginning of the problem — it is the first time it became visible. The patterns were forming long before. Here is what is quietly raising the financial stakes for your teenager right now, and three things you can do this week while the formation window is still open.

Why Financial Literacy Doesn't Change Student Behaviour

Schools across Singapore invest real time and resources in financial literacy education. The content is often solid. Yet the behaviour rarely changes. This article examines why, and what three specific design gaps are responsible — each with a practical resolution.

Are You Raising a Financially Mature Teenager, or Just a Supervised One?

Most parents believe that teaching a teenager about money means explaining it better. It doesn’t. True financial maturity happens when we shift from giving "supervised permission" to creating the conditions for real stewardship: responsibility, reflection, and honest consequences.

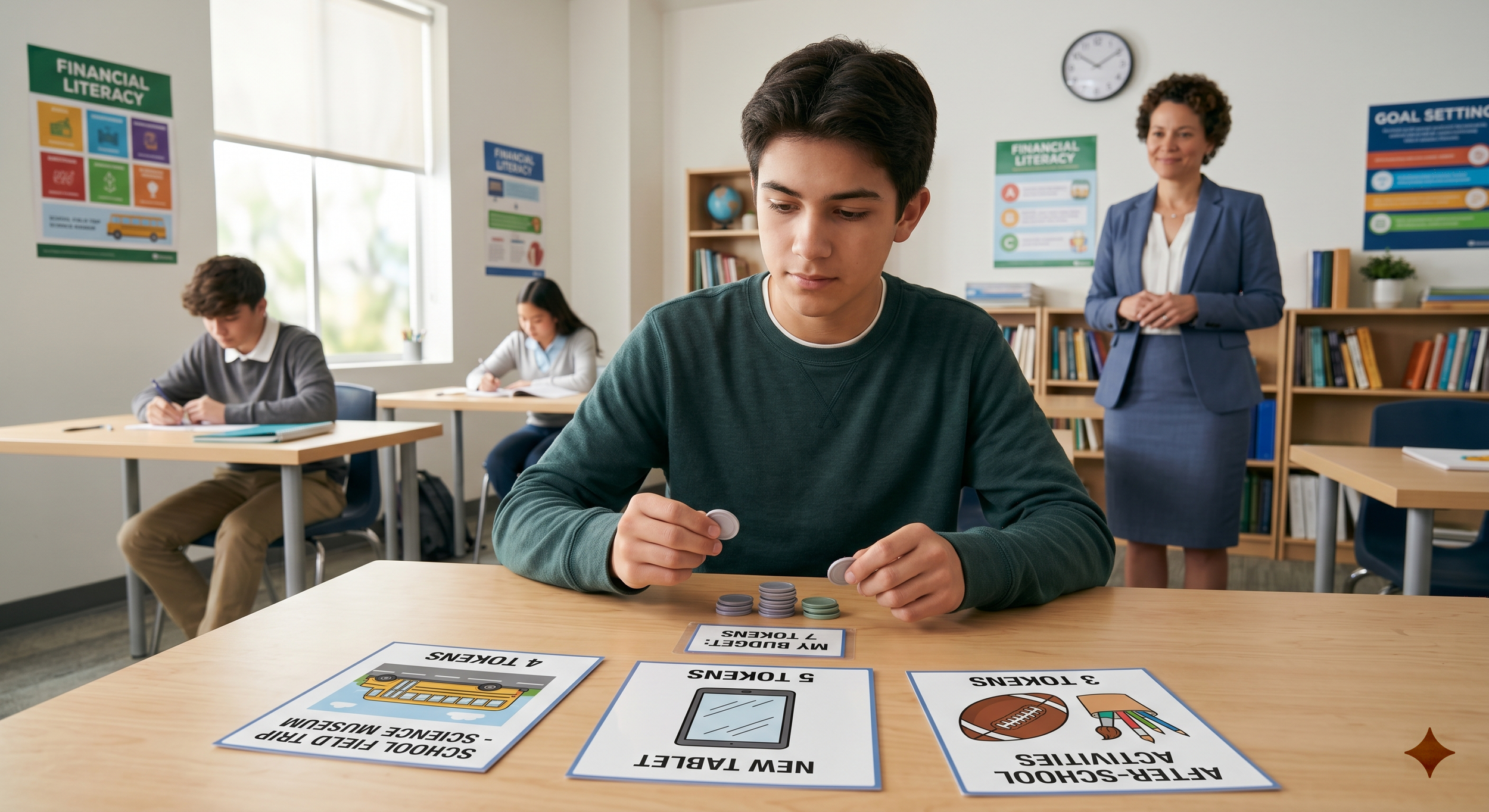

The Real Test of Financial Maturity Is What Students Do with Freedom

Most financial education programs focus heavily on lesson compliance and theoretical knowledge. But as Singaporean schools navigate structured curricula, a glaring gap remains between knowing money concepts and managing real-world assets. This article explores the Autonomy–Temptation–Choice Load framework and outlines how educators can bridge the gap from classroom financial literacy to actual student maturity.

Why Your Teenager’s Impulsive Spending Is Not a Knowledge Problem

Somewhere between primary and secondary school, a teenager's relationship with money undergoes a massive operational shift. It stops behaving like a simple medium of exchange and begins functioning as a social language. When a teen makes a spending choice that blindsides their parents, structural ignorance is rarely the culprit. Instead, the behavior is driven by a hidden psychological engine: The Identity-Spending Loop. Learn how to decode this loop and move your child from financial supervision to true financial maturity.

Closing the Consequence Gap: Why Protecting Students from Financial Mistakes is Sabotaging Their Maturity

We often think the safest way to teach a student about money is to protect them from making a mistake with it. However, when we remove the "sting" of a bad decision in the classroom or the canteen, we aren't protecting the student—we are dismantling their behavioral immune system. This article explores why educators must close the "Consequence Gap" to move students from supervised literacy to independent stewardship.

The High-Achiever Paradox: Why Financial Literacy Fails Without "The Maturity Margin"

We are producing students who are academically capable of passing a math test but biologically incapable of resisting an impulse. This article explores why the traditional "information-first" approach to financial literacy is failing and introduces a framework for building genuine maturity in a frictionless digital world.

Schools Are Mistaking Financial Knowledge for Financial Readiness

Students can know the right financial terms and still not be financially ready. That is because financial knowledge answers the question, “Do you know?”, while financial readiness answers a harder one: “Can you decide well when it actually matters?” If schools want financial literacy to prepare older youth for real-life autonomy, they need to design for judgement under pressure, not just correct explanation.

Why Financial Literacy Lessons Do Not Automatically Change Student Behaviour

Students can often explain sound money principles in class, yet make very different decisions when real choice, pressure, and trade-offs appear. The issue is often not a lack of knowledge, but a lack of behaviour formation. If schools want financial literacy to contribute to life readiness, they need to design not only for understanding, but for stewardship.

The Real Goal Was Never Financial Literacy

Many parents want children to learn financial literacy. But money was never the final subject. It was one of the earliest places where maturity became visible. Here are the 3 deeper areas young people need if we want them to become truly life-ready.

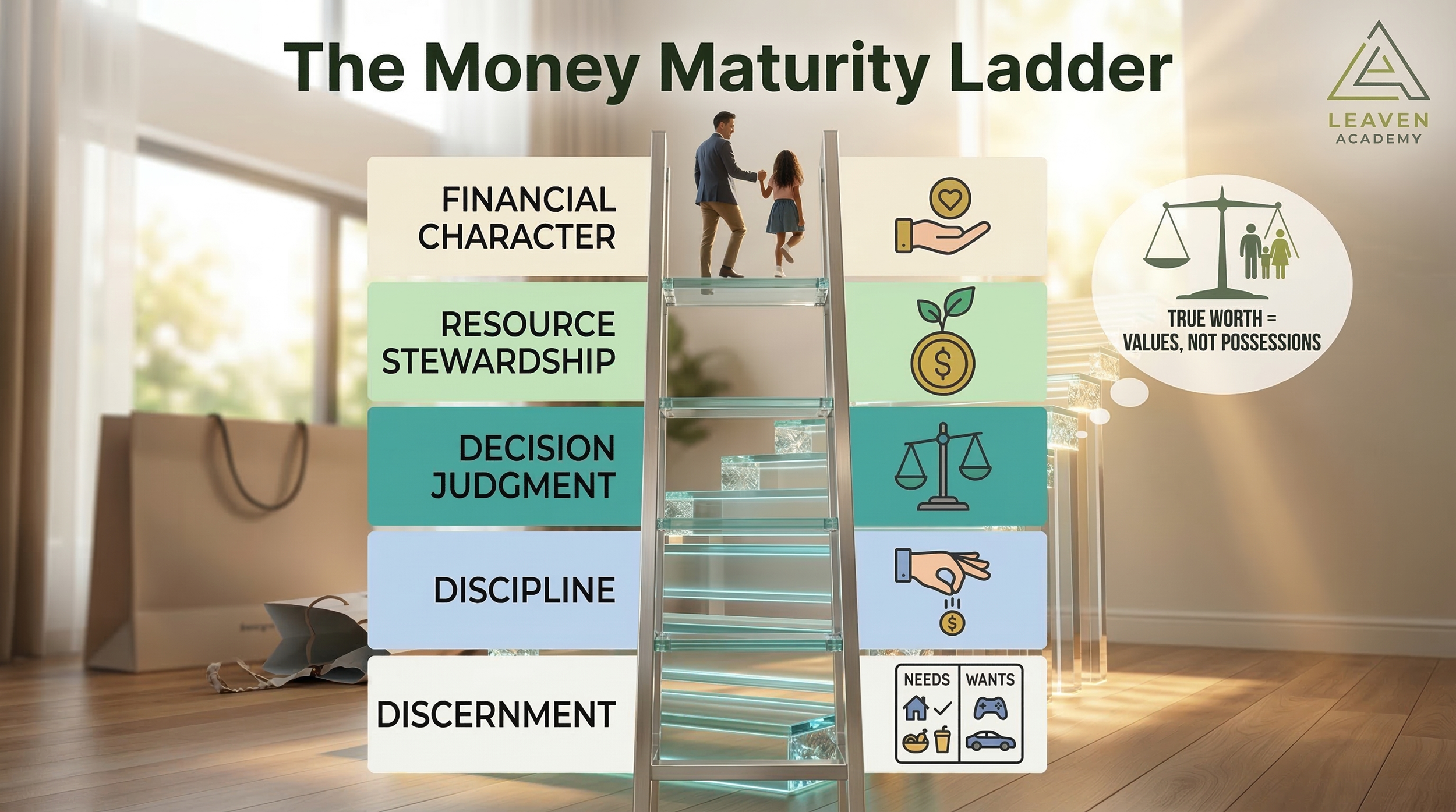

Is Your Child Financially Mature or Just Financially Supervised?

Learn how to tell if your child is financially mature or simply financially supervised using the Money Maturity Ladder and practical parent questions.

How Digital Spending Weakens Your Child’s Money Maturity (And What Parents Should Adjust)

Most parents think digital payments are neutral tools.

They are convenient.

They are trackable.

They speed things up.

But in my experience working with primary school children, the issue is not technology. It is friction.

When friction disappears, consequence disappears from the child’s emotional experience. And that is how a 9-year-old can casually say, “It’s my parents’ money. They will pay.”

What looks efficient today can quietly weaken money maturity long term.

This is not about banning Apple Pay, GrabPay, POSB watches, or gaming top-ups. It is about understanding the hidden developmental gaps created by frictionless systems.

If we understand these gaps clearly, we can adjust without overreacting.

Let me break this down structurally.