Is Your Child Financially Mature or Just Financially Supervised?

The Real Test of Whether a Child Understands Money

Many children appear financially responsible.

They follow instructions.

They stay within budget.

They buy what they are told to buy.

And as parents, it is very easy to look at that and feel encouraged.

We think, good, my child is learning to handle money well.

But in my experience, the real test is not what a child does when a parent is standing beside them.

The real test is what happens when supervision disappears.

Because that is when something interesting happens.

A child who behaves perfectly at the supermarket may spend impulsively the moment they walk past a convenience store after school.

So the real question is not, does my child know how to use money?

The real question is this:

Is my child financially mature, or just financially supervised?

This matters more than many parents realise, because good behaviour on the surface can sometimes be obedience rather than understanding. And if we want children to master money later in life, we need to know whether money wisdom is actually becoming internal.

In this article, I want to show you a simple framework I call the Money Maturity Ladder.

If you prefer to watch, here’s the full breakdown:

Why Supervised Behaviour Can Look Like Money Maturity

Over the years working with parents and children, I have noticed something very consistent.

Many parents tell me, “My child is very responsible with money.”

And often, that is true.

But only when the parent is present.

When parents are around, many children can behave very responsibly. They can buy groceries with a fixed budget, help to purchase food, follow the list, and carry out instructions properly.

And when you watch that happen, it looks like maturity.

But very often, what we are actually seeing is obedience.

The parent is deciding.

The child is executing.

That is not the same thing.

You can see this quite clearly around schools in Singapore. When parents are around, children often show restraint. But after school, the scene changes. They walk into convenience stores, buy slurpees, sweets, and snacks, and spend more freely.

The restraint was there when the parent was there.

But once the parent is gone, the decision changes.

That is why behaviour under supervision is not the same as maturity.

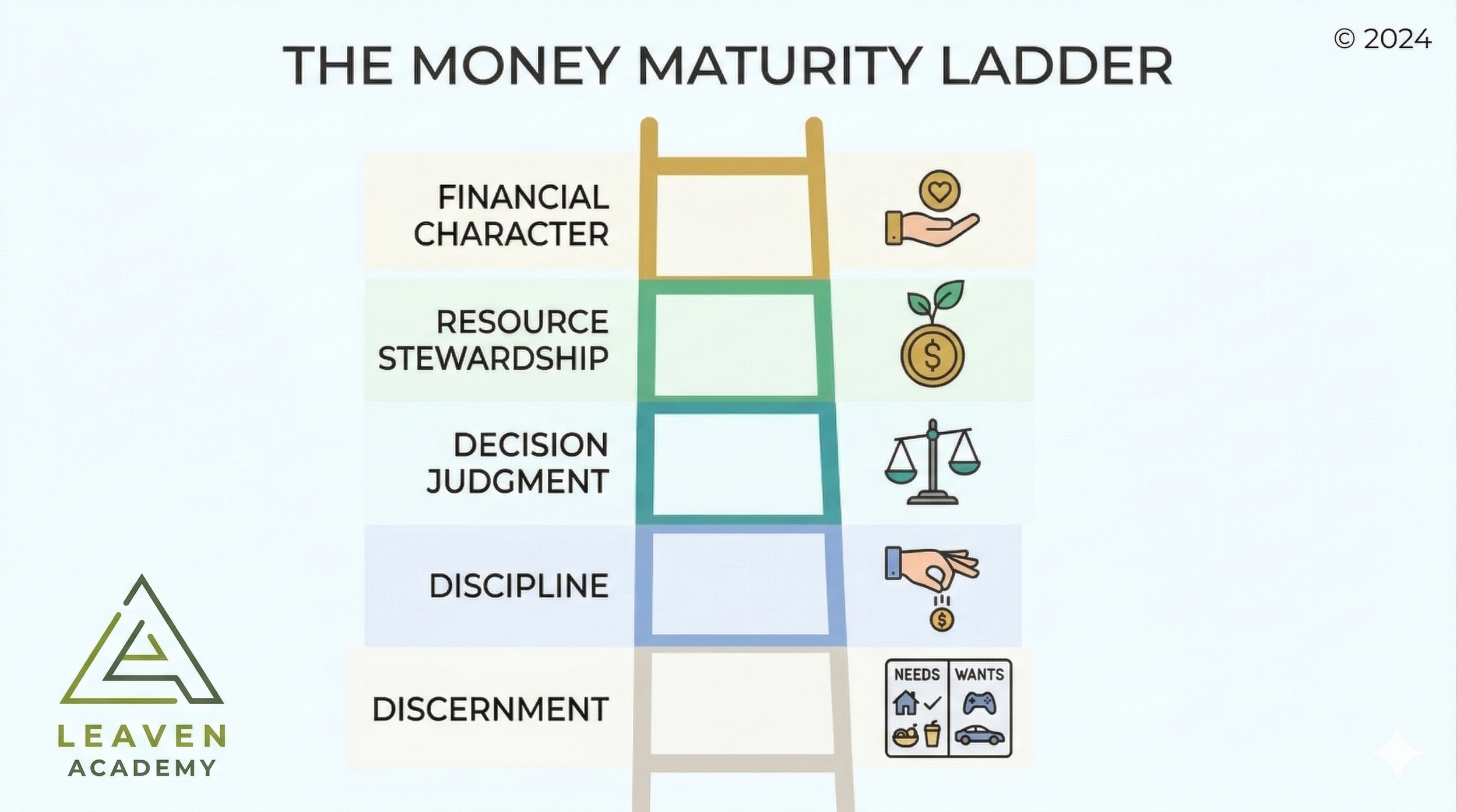

The Money Maturity Ladder

Financial maturity develops in stages.

It does not appear automatically just because a child gets older. It does not appear just because a child can count money. And it definitely does not appear just because a child can follow spending instructions.

It develops in layers.

I call this framework the Money Maturity Ladder.

The five stages are:

Discernment

Discipline

Decision Judgment

Resource Stewardship

Financial Character

These five stages help us see whether money understanding is becoming internal, or whether it is still being enforced from the outside.

And when children climb this ladder, money stops controlling them.

They begin controlling money.

A Simple Way to Test Your Child’s Financial Maturity

Here is a very simple way to observe where your child is.

Give your child ten dollars.

Then watch what happens.

Do not overcomplicate it. Just give your child a small amount of money and observe the decision that follows.

A very ordinary example is this: a child finishes school, walks past a convenience store, and decides whether to buy snacks after school.

That small moment tells you a lot.

Not because the purchase itself is huge, but because the thinking behind the purchase reveals something deeper.

After the purchase, ask four questions:

Why did you buy this?

Was it a need or a want?

What value did you get?

Did you consider any alternatives?

These questions are powerful because now you are not just observing the action.

You are examining the thinking.

Can your child explain the decision, or only the action?

That difference matters.

Because explanation reveals maturity.

Stage 1: Discernment

Discernment is the ability to know the difference between a need and a want.

This sounds basic, but many children are still blurry on it.

A meal during recess may be a need.

An extra snack, sweets, or a drink just because it looks nice is usually a want.

The point is not that wants are wrong. That is not the issue.

The real question is whether the child understands what kind of decision they are making.

For example, if a child buys sweets after school, the issue is not just the sweets. The deeper issue is whether the child understands that this was a want rather than a need.

Small purchases reveal big patterns.

Because if a child cannot identify a want when the amount is small, it becomes harder to make wise decisions when the amounts become bigger later.

One very practical thing parents can do is ask, “Was that a need or a want?” Then wait and let the child answer.

If you want a deeper breakdown of how to teach this clearly, read Teach Kids Wants vs Needs Properly:

https://www.leavenacademy.com/blog/teach-kids-wants-vs-needs

Discernment is where money maturity begins.

Stage 2: Discipline

The second stage is discipline.

This is the ability to resist impulse.

Even when children know something is a want, they often still want it immediately. That is normal. Children naturally lean towards instant gratification.

They see it.

They want it.

They buy it.

But discipline is the ability to pause.

To hold back.

To say, “I do not need to buy this right now.”

This becomes especially obvious when children receive pocket money for the first time. Sometimes, a child who has never had to control money before suddenly gets freedom in primary school, and then spends everything immediately.

Not because they are bad children.

Not because they are hopeless.

But because they have never practised control before.

They had supervision before.

Now they have freedom.

And freedom without preparation often turns into impulsive spending.

That is why small mistakes are useful. A child who spends too quickly and then has nothing left later begins to feel a consequence. And that consequence teaches something supervision never can.

If this is a recurring issue in your home, read How to Stop Child Impulse Buying:

https://www.leavenacademy.com/blog/how-to-stop-child-impulse-buying

Discipline grows through experience.

Stage 3: Decision Judgment

The third stage is decision judgment.

This is where children move beyond pure impulse and begin evaluating options before spending.

They start asking:

What are my choices?

Is there a better option?

Is this worth the price?

Could I wait?

Could I buy something else instead?

At this stage, spending becomes a decision rather than a reaction.

I remember a case where a child spent every cent at the school bookshop. Not because anything there was necessary, but because the child suddenly had the freedom to choose. Once that freedom appeared, everything became tempting.

The spending was not really about the items.

It was about the thrill of having power over money for the first time.

Many parents respond to this by tightening control immediately. They think, since my child made a poor choice, I must take over everything again.

But that does not build judgment.

It only restores supervision.

A better response is to guide the thinking. Ask what other choices were available, what made the purchase seem worth buying, and whether the child would make the same choice again.

Judgment improves through reflection.

Stage 4: Resource Stewardship

The fourth stage is resource stewardship.

This is when children begin to understand that money must last.

Many children think about money only in the present.

“I have money now, so I can spend now.”

But stewardship teaches a child to think further ahead.

How long do I want this money to last?

Do I want to use all of it today?

What happens tomorrow if I spend everything now?

Can I save part of it?

Can I delay this purchase?

This is where patience begins to form.

Parents can help by asking one very simple question:

How long do you want this money to last?

That question changes the frame.

Now the decision is no longer just about the item. It becomes about time, planning, and preserving a resource.

Short-term pleasure or long-term usefulness?

That is the tension.

And when children learn to sit inside that tension and make a thoughtful choice, stewardship begins to grow.

Stage 5: Financial Character

The fifth stage is financial character.

This is where money maturity becomes deeper than just spending habits.

Because money is not only about buying.

It is also about values.

Does your child only think about spending?

Or do they also think about saving and sharing?

Do they show gratitude?

Do they think beyond themselves?

Do they understand that money can be used wisely not just for personal enjoyment, but also with consideration for others?

A child with financial character does not simply ask, “What can I get?”

They also begin to ask, “What should I do with what I have?”

That is a very different mindset.

And it matters because character is what holds the whole ladder together.

Character completes maturity.

What Parents Can Do This Week

You do not need a complicated lesson.

Start with these three steps:

Give your child a small amount of money regularly.

Not a huge amount. Just enough for practice.Allow small mistakes.

Do not rescue every poor decision immediately.Discuss decisions after they spend.

Ask:Why did you buy that?

Was it a need or a want?

What value did you get?

Did you consider another option?

The real gold is not only in the purchase.

It is in the conversation after the purchase.

That is where the child learns to think, explain, and reflect.

And that is where internal maturity starts to form.

Common Mistakes Parents Make

Mistake 1: Confusing obedience with maturity

A child who follows instructions well is not automatically financially mature.

Mistake 2: Rescuing every poor decision

If parents remove every consequence, children do not learn from mistakes.

Mistake 3: Focusing only on behaviour, not thinking

The real issue is not just what the child bought, but why they bought it.

Mistake 4: Tightening control after every mistake

More supervision may create compliance, but not judgment.

Frequently Asked Questions

How can I tell if my child is financially mature?

Watch what your child does with money when you are not directing every step. Independent decisions reveal far more than supervised behaviour.

What is the Money Maturity Ladder?

It is a five-stage framework: discernment, discipline, decision judgment, resource stewardship, and financial character. It helps parents see whether money understanding is becoming internal.

Should I let my child make money mistakes?

Yes, within small and safe limits. Small mistakes teach consequences while the stakes are still low.

What should I ask after my child makes a purchase?

Ask why they bought it, whether it was a need or a want, what value they got, and whether they considered alternatives.

Is financial maturity the same as financial knowledge?

No. A child may recognise money and count it well, yet still make poor decisions. Financial maturity is decision capability, not just knowledge.

Conclusion

Financial maturity is not revealed when parents are watching.

It is revealed when children make decisions alone.

That is when the truth comes out.

Discernment.

Discipline.

Decision judgment.

Stewardship.

Character.

These are not just ideas.

They are signs.

They reveal whether your child is merely following instructions, or whether your child is actually learning to master money.

If your child made a purchase today, could they clearly explain why they made that decision?

Because if they cannot explain the reasoning, your child may still be financially supervised rather than financially mature.

If you want to go deeper into the full developmental framework, the next step is to explore the Money Maturity Ladder as a whole and how children move through it stage by stage.

Related articles:

Teach Kids Wants vs Needs Properly

https://www.leavenacademy.com/blog/teach-kids-wants-vs-needsHow to Stop Child Impulse Buying

https://www.leavenacademy.com/blog/how-to-stop-child-impulse-buying

If you are a parent looking to bring financial literacy to your child through an experiential workshop, you can recommend us to your school, by sending them our webpage. We conduct financial literacy programmes for schools in Singapore.