Why Money Behaviour Reveals More Than Money Habits

Most schools treat financial education as a subject. But the way students handle money is one of the clearest windows into how they handle responsibility more broadly. This article introduces the Maturity Signal Framework and explains what student money behaviour is actually telling schools — and what to do about it.

Are You Raising a Financially Mature Teenager, or Just a Supervised One?

Most parents believe that teaching a teenager about money means explaining it better. It doesn’t. True financial maturity happens when we shift from giving "supervised permission" to creating the conditions for real stewardship: responsibility, reflection, and honest consequences.

The Real Test of Financial Maturity Is What Students Do with Freedom

Most financial education programs focus heavily on lesson compliance and theoretical knowledge. But as Singaporean schools navigate structured curricula, a glaring gap remains between knowing money concepts and managing real-world assets. This article explores the Autonomy–Temptation–Choice Load framework and outlines how educators can bridge the gap from classroom financial literacy to actual student maturity.

Closing the Consequence Gap: Why Protecting Students from Financial Mistakes is Sabotaging Their Maturity

We often think the safest way to teach a student about money is to protect them from making a mistake with it. However, when we remove the "sting" of a bad decision in the classroom or the canteen, we aren't protecting the student—we are dismantling their behavioral immune system. This article explores why educators must close the "Consequence Gap" to move students from supervised literacy to independent stewardship.

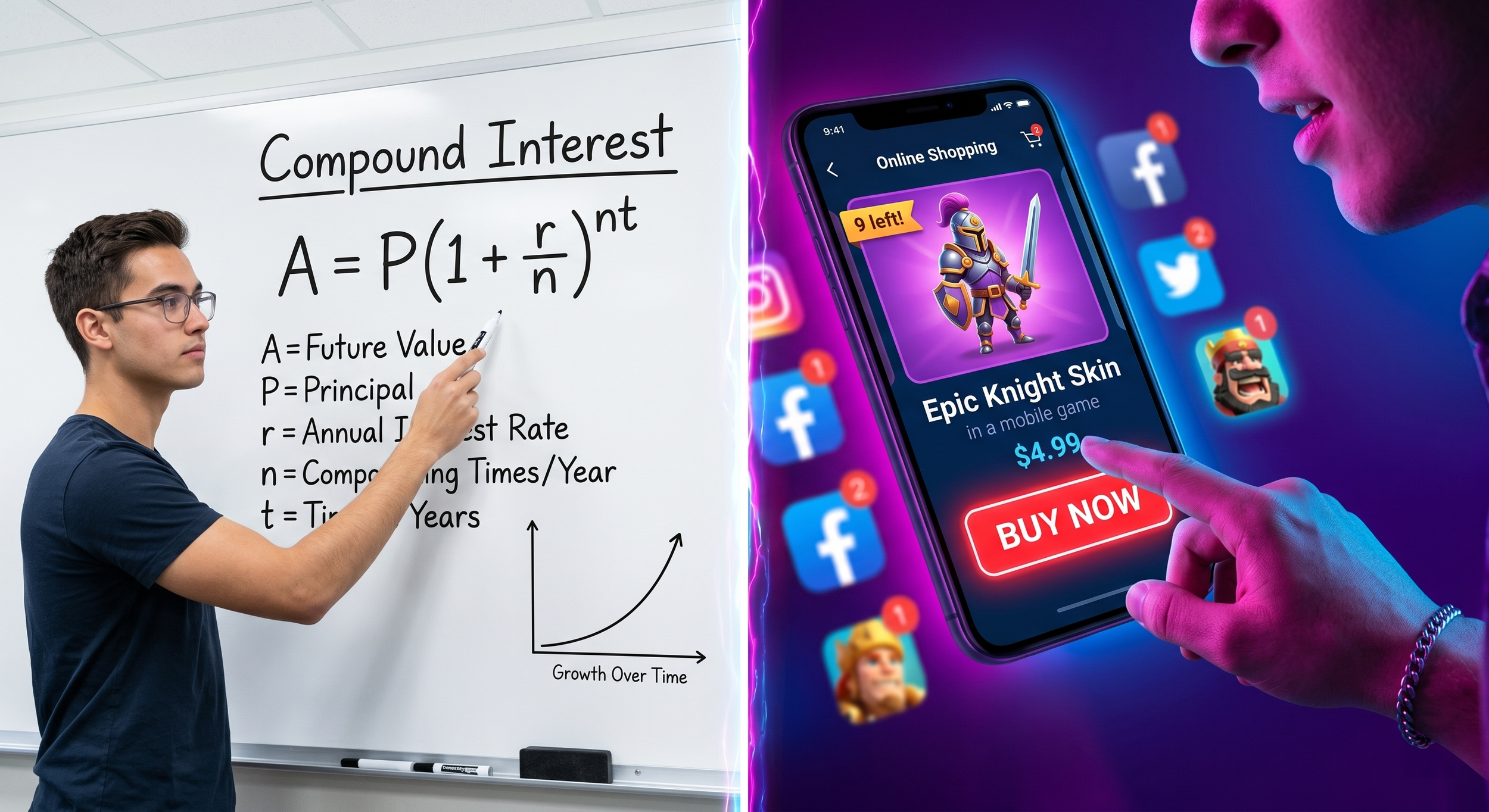

The High-Achiever Paradox: Why Financial Literacy Fails Without "The Maturity Margin"

We are producing students who are academically capable of passing a math test but biologically incapable of resisting an impulse. This article explores why the traditional "information-first" approach to financial literacy is failing and introduces a framework for building genuine maturity in a frictionless digital world.

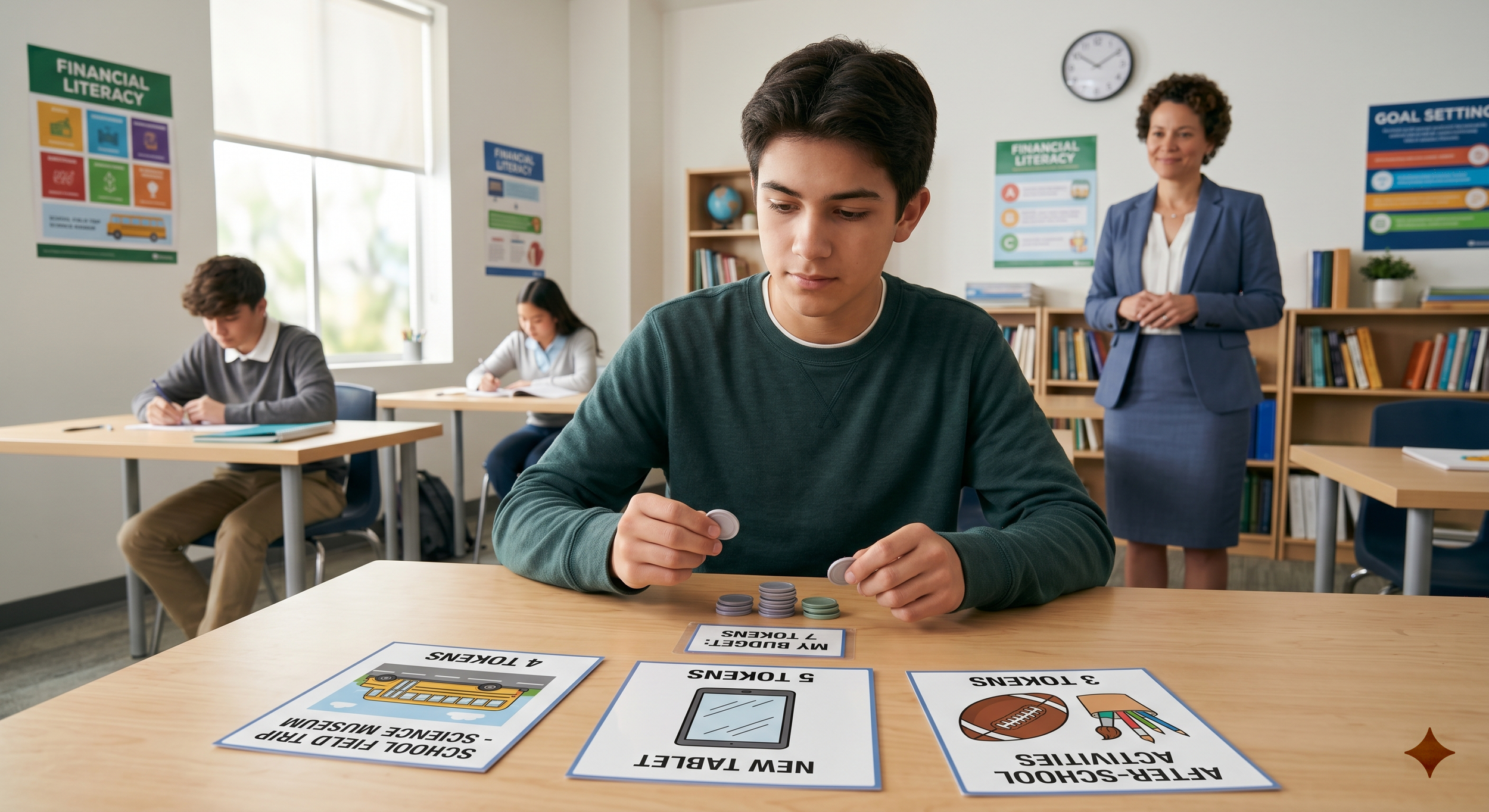

Why Financial Literacy Lessons Do Not Automatically Change Student Behaviour

Students can often explain sound money principles in class, yet make very different decisions when real choice, pressure, and trade-offs appear. The issue is often not a lack of knowledge, but a lack of behaviour formation. If schools want financial literacy to contribute to life readiness, they need to design not only for understanding, but for stewardship.